Credit Card Surcharges vs Cash Discounts vs Dual Pricing: What’s the Difference?

When it comes to running a business, merchants can often be stuck between a rock and a hard place when it comes to allowing customers to use credit cards.

On the one hand, customers want the flexibility to use credit cards wherever they make a purchase. In fact, they expect all merchants to allow them to use a credit card. They also don’t want to have to pay to use their credit card.

On the other hand, card associations charge merchants per credit card transaction made in their stores. Unfortunately for merchants, there’s no way to recoup those costs apart from passing those charges onto their customers.

This isn’t a new discovery. Surcharges had been prohibited against the card brand rules, which were modified in 2013 due to a settlement agreement. View the settlement details at https://www.paymentcardsettlement.com/en

In this article, we’ll discuss how merchants and credit card companies deal with surcharges, how alternative like a cash discount can be used, and the main differences between the two.

What Is a Surcharge?

Let’s start with the basics.

A surcharge is a fee that vendors can add onto credit card transactions to make up the cost they’re charged by the credit card association. Debit cards cannot be surcharged. Each card association has its own guidelines for applying surcharges.

A surcharge is a fee that vendors can add onto credit card transactions to make up the cost they’re charged by the credit card association.

A card association is the network of banks that process payment cards of a specific brand. These are brands you know like Visa, MasterCard, Citi, and American Express. Many of these associations will co-brand their cards with other banks, airlines, or hotels.

In most cases, card associations cap their surcharges up to 3% for the transaction value. Many merchants, however, tend to charge a flat fee for their surcharge whether it falls under that threshold or not.

How to Enroll

If you’re a merchant wanting to enroll with a card association to allow credit card surcharges at your place of business, you’ll find it’s not an incredibly easy process.

First, you have to know which states allow surcharges and which don’t. We’ll discuss this briefly under limitations.

Next, you have to look at all the credit cards your business accepts – Visa, MasterCard, Amex – and explore their surcharge guidelines. Each card provider will have a set of requirements that you should meet before you apply to add a surcharge. In most cases, the credit card company will ask you to provide the following:

- Business name

- Contact information (email, address, phone number)

- Number of locations applying for surcharging

- Channel type (brick & mortar, eCommerce, mail order, etc.)

- Type of surcharge (usually brand or product)

In most cases, the credit card company will ask you to provide your business name, contact information, channel type, type of surcharge.

You have to provide no less than 30 days’ notice to the credit card company and your merchant’s acquirer that you intend to impose surcharges on your transactions.

Compliance Requirements

You’ll notice card associations DO NOT want you to discourage customers from using credit cards in favor of cash or debit options. That being said, most of the guidelines card associations provide are the same:

- There is 3% limit.

- Post appropriate surcharge signage in your store about credit options. Have several signage points like on your business’ door, around the shop, and at the point of sale.

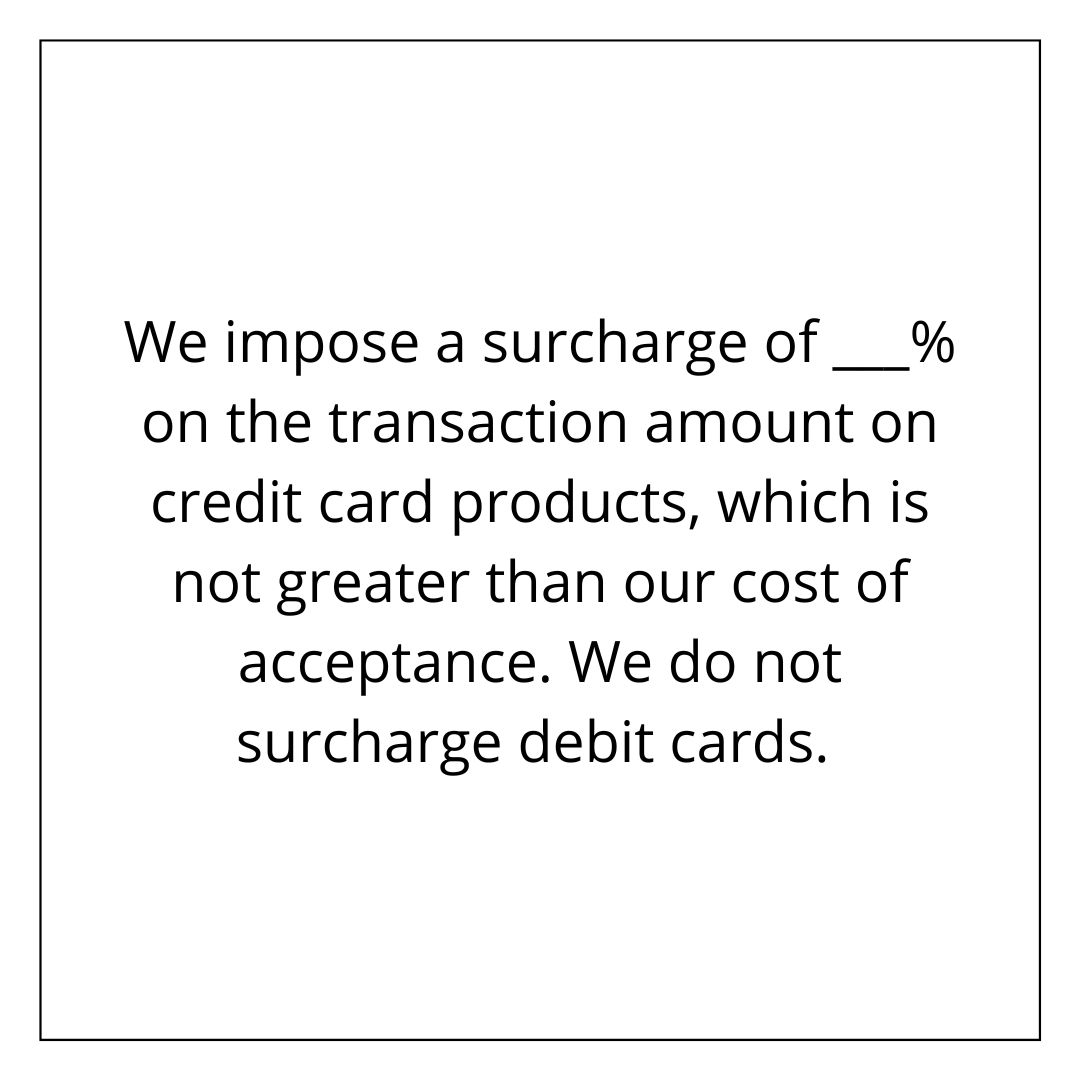

Example of cash discount signage:

“We impose a surcharge of ___% on the transaction amount on credit card products, which is not greater than our cost of acceptance. We do not surcharge debit cards.”

Download surcharge signage pdf example.

- Include surcharge as a separate line on your receipts. This means you need a POS that can handle this.

- Choose between applying brand-level surcharges or product-level surcharges – can’t do both.

- Notify card association and your ISO in writing at least 30 days in advance.

You also need to comply with state laws regarding surcharges.

Limitations to Surcharges

There are some limitations to adding surcharges to your credit card transactions. For starters, if you own a business in one of the following states, you cannot legally charge customers surcharges for using a credit card, according to Visa:

- Colorado

- Maine

- Oklahoma

- Connecticut

- Massachusetts

In these states, your option to recoup your cost charged by the credit card companies is to offer a cash discount for those who pay by cash or check rather than by credit card. If you have a multi-state business, you can apply surcharges in states where it is legal and encourage cash discounts in states where you cannot legally surcharge.

Another limitation of surcharges is that you cannot add a surcharge on debit card transactions. Surcharges may only be applied to credit card transactions. This provision – the Dodd-Frank Wall Street Reform and Consumer Protection Act – became law in 2010.

What is a Cash Discount?

If you live in a state where surcharging is illegal or you don’t want to jump through the hoops to set up your business for surcharges, offering a cash discount might be a prudent route for your business.

A cash discount is just what it sounds like; you offer a discount to customers who pay with cash or check. The idea here is that at the time of sale, when a customer pays with cash, they receive a discount off the regular sales price. When a customer pays via a payment type other than cash at the time of sale, they do not receive any discount for the transaction.

A cash discount is just what it sounds like; you offer a discount to customers who pay with cash or check.

Pros of Cash Discounts

There are many benefits associated with offering a cash discount. First, you provide customers with an incentive to pay with cash.

The second is that offering a cash discount can make many customers happy. They walk away having gotten a chance to save a little money. Sometimes, offering a cash discount can mean the difference between making the sale and not, especially for smaller stores.

Third, you don’t have to jump through so many hoops to set up a cash discount. The discounts you set are primarily up to your discretion.

Cons of Cash Discounts

While there are a good number of advantages to offering a cash discount, there are some drawbacks you need to consider.

The major drawback is that people tend to spend more when they pay with a credit card. Because people cannot see the money physically leaving their wallets, they’re more likely to add another item or two onto their purchase.

Cash Discounts Compliance

While you don’t have the same hoops to jump through with cash discounts as you do with surcharges, there are some items you need to be aware of to run a compliant cash discount for your business.

First, you must provide a signage before the transaction is made regarding cash discounts. Have several signage points like on your business’ door, around the shop, and within the POS system.

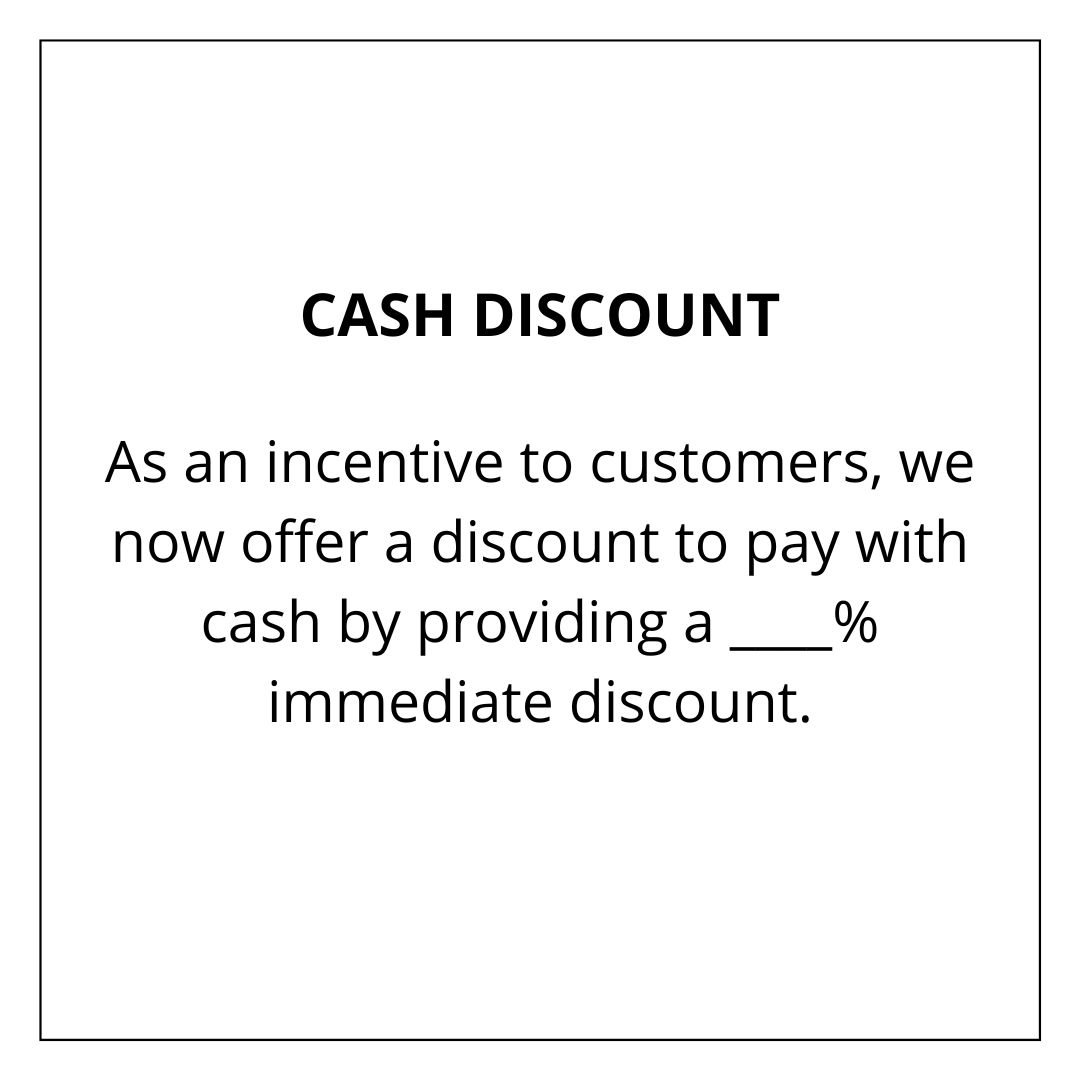

Example of cash discount signage:

“As an incentive to customers, we now offer a discount to pay with cash by providing a 4% immediate discount.” Download Cash discount signage.

Second, you must present the customer with a detailed receipt showing the cash discount information for the transaction.

Third, know the laws for the state you’re in. Most of the states where it’s illegal to surcharge encourage businesses to offer cash discounts. Before starting any cash discount program, consult your state’s law.

What is Dual Pricing?

Dual pricing is essentially similar to a cash discount, but instead of displaying a discount at checkout, it involves displaying two prices upfront: one for cash payments and one for card payments.

Purpose: Provides transparency by clearly showing the difference in cost between payment methods.

Key Features:

- Both prices (cash and card) are displayed at the point of sale.

- The card price is higher, while the cash price is lower.

- Ensures customers are aware of their payment options and the associated costs.

- Legal in all states, and compliant with card brand guidelines when implemented properly

Example: A product is labeled $100 for cash payments and $103 for card payments. Customers choose their preferred payment option based on the pricing displayed.

What’s the Difference?

When you first dive into surcharges vs. cash discounts vs dual pricing, you likely think they sound very similar.

The key difference between surcharges and cash discounts is that with surcharges, you are adding a fee to credit card transactions, while with cash discounts, you are providing a discount off the advertised sales price when customers pay with cash.

For some businesses, surcharges and cash discounts or dual pricing are two halves of the same whole. Merchants can use one or another to incentivize customers to transact with them in a way that results in lower costs for the vendor.

The key difference between surcharges and cash discounts or dual pricing is that with surcharges, you are adding a fee to credit card transactions, while with cash discounts, you are providing a discount off the advertised sales price when customers pay with cash, with dual pricing you display 2 prices – cash and card.

In addition, surcharges are much more regulated and require an authorization with the credit card companies. Businesses can be much more autonomous when setting up cash discounts or dual pricing and have fewer rules they need to worry about when they do so.

Final Thoughts

Before deciding on a surcharge, cash discount or dual pricing for your business, take a look at your books. Are you getting a lot of customers who pay with a credit card? How much does that account for in fees that you need to pay to the credit card company?

Also, consider your customers. Would they react ok to a surcharge or would they be appalled? Could you make more sales if you offer a cash discount? Will that cash discount degrade your margins too much?

These are all questions you should ask yourself before deciding which route is best for you. If you need help deciding, consult with other business owners and consultants to help you make an informed decision.

Additional Resources

– Free Processing program – https://ehopper.com/free-processing/

– Merchant surcharge rules from Master Card details…

– Merchant surcharge rules from Visa details…

– Test drive eHopper POS for free.

– eHopper POS Surcharge feature https://ehopper.com/surcharges/

– eHopper POS Cash Discount feature https://ehopper.com/cash-discount-program/

Disclaimer: The above is for information purposes only. eHopper is not liable for any non-compliance with rules and regulations arising out of your use of this program.