What are Merchant Services and How it Works (Guide)

As a new business owner, are you looking to accept any transaction type for payments other than cash and paper check? If so, getting started with a merchant services account will be one of the most crucial elements of setting up your business.

In brief, merchant services are all of the products, services, and technology that allow your business to securely process card transactions, and receive the payment into your bank account. These card transactions may include credit cards, debit cards, online payments, and contactless payment options such as Apple Pay and Google Pay.

Essentially, without merchant services, it would be impossible to accept card transactions or receive funds from these transactions.

That is why, as a business owner, it is so important to understand and become familiar with exactly what merchant services is and how it works, so you can make the best decisions possible for when it comes time to open up your business and start making money.

What are Merchant Services?

As touched upon above, merchant services are composed of all the tools that allow your business to accept credit cards, debit cards, and any other form of electronic payment, and then safely and securely send the funds over to your bank.

It is important to make the right decision for your business on these these tools, as the ones you choose to make up your merchant services will determine how you accept payments, the type of payments you accept, and how fast and secure those payments are.

Included in the tools that are comprised of merchant services are a merchant service provider, payment gateway, merchant acquiring bank, credit card terminals, and point-of-sale (POS) software, all of which are critical for the process of seamless card transactions to occur.

One of the first steps for obtaining merchant services is to get started with a merchant service provider. A merchant service provider, or MSP, is a company that provides businesses with the tools and setup necessary to seamlessly and securely accept card payments.

Having a MSP is critical as it is the facilitator between your business, your customers, and the banks, enabling funds from your customers’ cards to securely and successfully be sent to your bank account.

How Does Merchant Services Work?

Though they may appear to occur instantaneously, card transactions actually comprise of a very multi-layered process, with many moving parts behind the scenes.

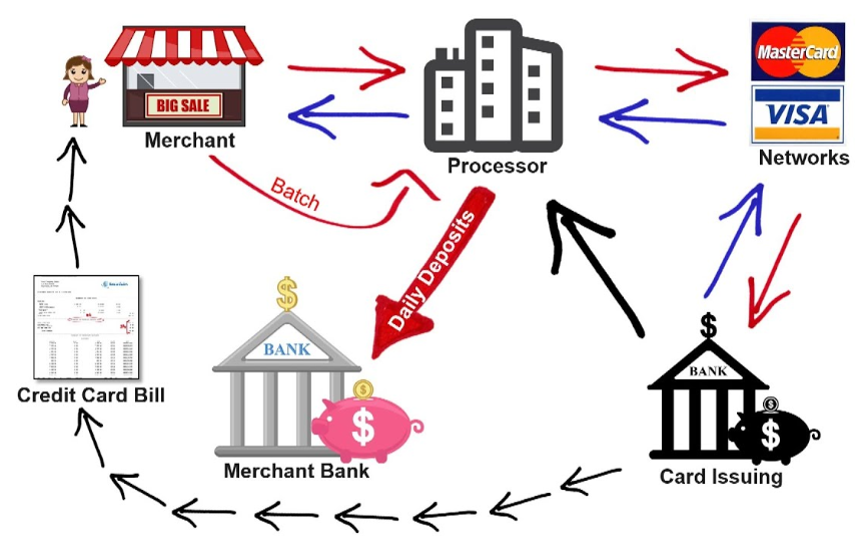

The process, which begins when a customer provides his card and is complete when the funds are deposited into your account, occurs in 3 steps: authorization, clearing and settlement. Each of these steps involves an exchange of transaction data and funds that need to be settled and balanced.

Merchant services flow, at a glance

Step 1: Authorization

During this step, the customer/cardholder presents their credit card to you, the merchant, which will be read by a credit card processing terminal, through the use of a point of sale system. Alternatively, the card can be read via an online gateway through an online ordering platform.

The card’s information is then sent to the acquiring bank (the bank that facilitates your merchant account), which sends those details through the credit card network (Visa, MasterCard, etc.) to the card issuing (customer’s) bank.

The customer’s bank will then either approve or decline the transaction, based on the card data it receives, through an authorization code. This code will then be sent back through the credit card network and merchant acquirer to the credit card terminal/online gateway, and finally to the point of sale or online ordering system, which will allow for the completion of the purchase. This entire process occurs in just seconds.

Step 2: Clearing

In this step, transaction data that was processed through the merchant acquiring bank will be sent to the customer bank so it can be posted on the customer’s monthly credit card statement.

If you and the cardholder use different currencies, the transaction will be collected by the acquiring bank in your currency and sent to the customer bank in their currency.

Step 3: Settlement

In the third and final step, funds from the credit card transaction are paid and collected in the following manner: the customer bank bills the cardholder and then pays the merchant acquiring bank, which then pays you, the merchant, for the transaction by depositing the funds into your merchant account.

Understanding Merchant Services Fees

When choosing a merchant service provider, it’s important to understand the different fees associated with payment processing. Here are some of the most common fees you may encounter:

Transaction Fees: This fee is charged for each transaction processed through your payment system. Transaction fees typically range from 1-3% of the transaction amount, depending on the type of card and the payment processor.

Monthly Fees

Some merchant service providers charge a monthly fee for using their payment processing services. This fee can range from a few dollars to several hundred dollars, depending on the provider and the services offered.

Authorization Fees

Authorization fees are charged each time a transaction is authorized. This fee can range from a few cents to a few dollars, depending on the provider.

Chargeback Fees

If a customer disputes a transaction and requests a chargeback, the merchant may be charged a fee by the payment processor. This fee can range from $10 to $50 per chargeback.

PCI Compliance Fees

Payment Card Industry (PCI) compliance is required by all merchants who process credit card transactions. Some providers charge a fee for ensuring that your payment processing system is compliant with PCI standards.

Equipment Fees

Some providers charge a fee for the equipment needed to process payments, such as a credit card terminal or mobile card reader.

Early Termination Fees

If you cancel your contract with a merchant service provider before the end of the agreement, you may be charged an early termination fee. This fee can range from a few hundred dollars to several thousand dollars, depending on the provider and the terms of the contract.

Monthly Minimum Fees

Some providers require a minimum monthly processing volume. If you do not meet this minimum, you may be charged a monthly minimum fee.

Statement Fees

Statement fees are charged for the cost of sending monthly statements detailing your payment processing activity.

Gateway Fees

Gateway fees are charged for using the payment gateway to process online payments.

Retrieval Request Fees

If a customer requests a copy of a receipt or transaction record, you may be charged a retrieval request fee.

Voice Authorization Fees

Voice authorization fees are charged when a transaction is authorized over the phone.

Batch Fees

Batch fees are charged when you submit a batch of transactions for processing.

AVS Fees

Address Verification System (AVS) fees are charged for verifying the billing address of a credit card.

IRS Reporting Fees

Some providers charge a fee for filing IRS 1099-K forms for your payment processing activity.

It’s important to carefully review the fee schedule provided by your merchant service provider before signing up for their services. Be sure to ask about any additional fees that may not be listed on the fee schedule, and negotiate to have fees reduced or waived whenever possible. By understanding the fees associated with merchant services, you can better manage your expenses and make informed decisions about which provider to choose.

What POS Software to Use

Choosing the right point of sale software to go along with your merchant service provider is an essential step in starting your business and processing card transactions.

With a modern, cloud-based point of sale, such as eHopper, you are able to quickly take customer orders and process card transactions, while also recording the sales, inventory, and customer data from each transaction.

When you select Credit Card or Debit Card as the tender type in the point of sale, the transactional data will instantly be sent to the integrated credit card terminal at your business. The merchant then simply swipes or inserts his card into the terminal and the payment is processed (if approved by the issuing bank). The payment data will then be sent from the terminal back to the POS, for record keeping.

Within eHopper reporting, you are able to view all sales and order data from these transactions, including the tender type used, whether the transaction was approved or declined, and the card authorization code.

With POS software such as eHopper, you can also take card payments via an online ordering platform, which will be described in more detail in the section below.

How Do I Use Merchant Services Online?

You can connect your merchant account to not only your physical card readers at your store, but also to an online ordering site, so you can accept card payments virtually on the internet, providing a new (and more large scale) venue for you to take orders and make more revenue.

You can accept credit card payments online, through an online ordering system like eHopper.

To do this, you can set up your site with a virtual gateway, such as Authorize.net, which supports all major credit card networks. In addition, Authorize.net is one of the most secure payment gateways on the market, so you and your customers can feel confident that their payment data will be protected online.

If you do not yet have an account with a gateway such as Authorize.net, you can easily set one up through your merchant service provider. Other examples of payment gateways for accepting online payments include PayPal and Stripe.

All this and more can be achieved with the eHopper online ordering system. With eHopper online ordering, you will be able to quickly create an online shopping cart that fully synchronizes with your point of sale account, so that when orders are placed online (either through credit card or for future payment), all order info will appear in your POS, and inventory stock will be updated.

Using Merchant Services with eHopper

eHopper offers a number of exciting merchant service programs that you can take advantage of, namely the Free Processing and Free POS programs, which we will dive a bit deeper into in the sections below.

Alternatively, if you would like to have integrated payments with eHopper but stick with your existing merchant service provider, you are able to do this as well, but without obtaining the benefits of the Free Processing and Free POS programs.

Free Processing

The average processing rates for running credit card payments are 2.5% +$0.15 per transaction. With the eHopper Free Processing program, you can completely eliminate these fees, processing credit cards at a rate of 0%, with no additional fees or commitments. And yes, it is 100% legal!

Not only that, but if your business is approved for the program, you will receive completely free point of sale software, with either the eHopper Freedom or Restaurant Plan (usually $29.99/mo and $39.99/mo respectively), as well as a free PAX S300 credit card terminal that integrates with the eHopper software, and full support.

Getting started on this offer simply involves signing up for a cash discount or surcharge program, which we will explain in more detail below.

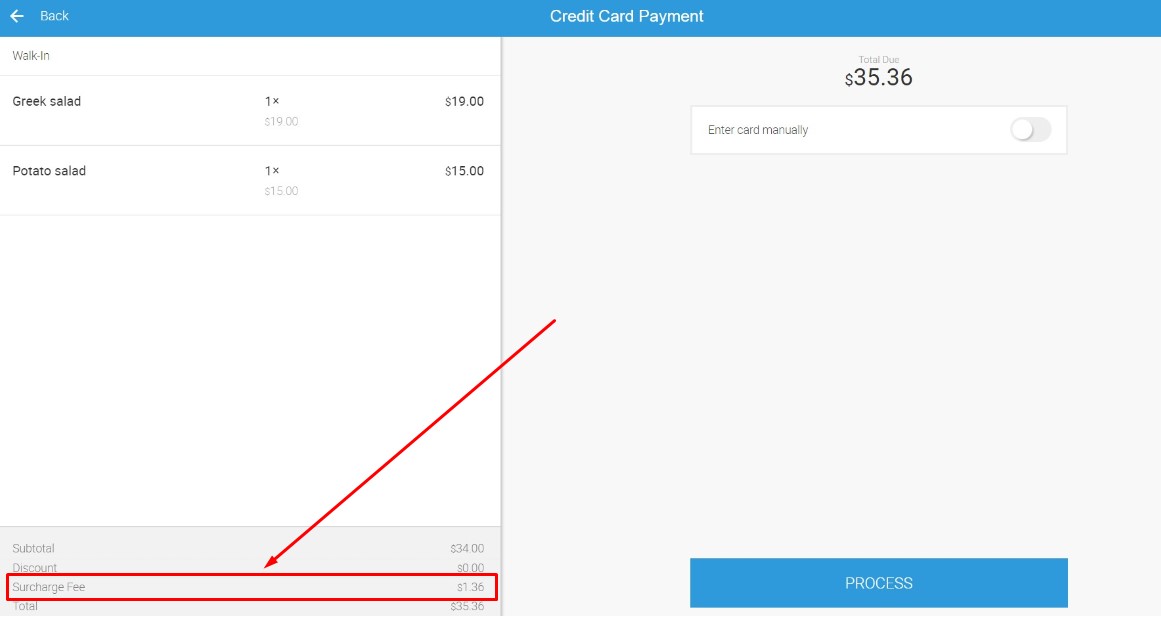

What is a Surcharge?

Surcharges allow you to completely eliminate your credit card processing fees by pushing the fees on to your customers who pay with credit card. When using a credit card, an additional fee at the rate of what your processing fee would have been, will be instantly added to the customer’s transaction total.

Credit Card Surcharge

Please note that surcharging is currently illegal in 10 states: Colorado, Connecticut, Kansas, Maine, Massachusetts, Oklahoma. California, Florida, New York, and Texas.

In addition, to sign up for the surcharge program, an application must first be submitted to your credit card company (Visa, MasterCard, etc) in order to qualify.

Businesses that would like to use the program should refer to the specific rules of their credit card company for any additional requirements, including consumer disclosure rules.

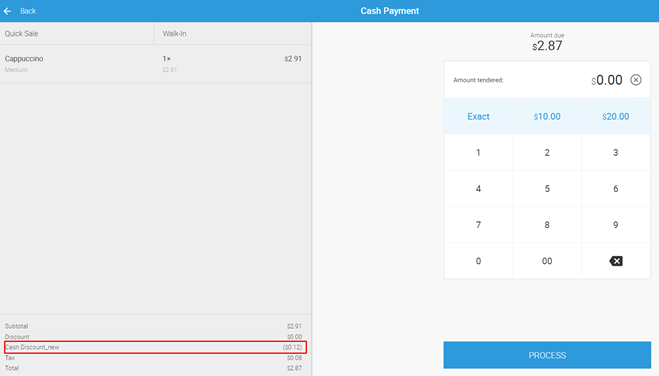

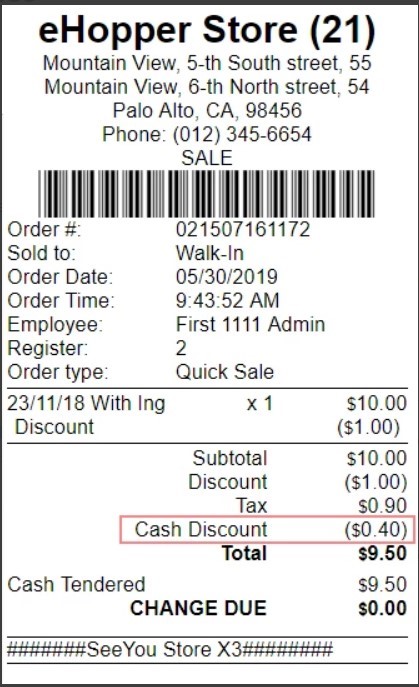

What is a Cash Discount?

Though they both work to offset your credit card processing fees, cash discounting differs from surcharges program in that instead of an extra fee being charged to customers who pay with credit cards, a discount is provided to customers who pay in cash, from the listed sales price of your products or services, with the discount amount equaling your card processing rates.

Cash Discount – Cash Transaction

If a customer were to pay with a tender type other than cash at the time of sale, they will not receive the discount and will be charged the listed sales price.

In order to not lose money when customers pay in cash, it is recommended to raise your listed sales price by the rate of your credit card processing fees. This way, when the discount is provided to customers who pay in cash, their resulting total will be the same as what it would have been without this program.

Aside from saving money on credit card processing fees, the cash discount program also gives your customers an incentive to pay in cash and allows them to leave more satisfied, knowing that they received a discount. Customers tend to like the feeling that they saved some cash.

The cash discount program is easy to set up and, unlike the surcharge program, is legal in all US states. The only requirement is that you disclose to your customers about the cash discount program at the point of entry (through signage at your establishment) and at the point of sale (on the receipt).

The good news is eHopper takes care of the disclosure at the point of sale by automatically adding the discount to customers’ receipts when they pay with cash.

Cash Discount Receipt

Free POS

If you prefer to not use surcharges or cash discounting, another option is to sign up with eHopper’s Free POS program.

Similar to the Free Processing program, if approved, you will also receive fully free POS software, with the Freedom or Restaurant Plan and a free integrated credit card terminal. The difference is, instead of using surcharging or cash discounts, you will be on eHopper’s low, flat merchant processing rates of 2.39%+10c per swipe or dip.

eHopper will also waive a $19.99 minimum fee when you process at least $2,000 a month in credit or debit card transactions.

Conclusion and Next Steps

As outlined in this guide, merchant services is a combination of the products, services, and tools that allow your business to run credit cards, debit cards, and other forms of electronic payment transactions, as well as retrieve those funds into your bank account at the end of the day.

It all amounts to a complex, multi-layered process with many moving parts and parties involved, yet the transactions that take place as a result of it, occur instantaneously.

Getting set up with merchant services is an essential step in starting your business, as without it, you will not be able to make money on customer credit card transactions, highly limiting your potential revenue.

With eHopper’s payment processing programs, you can save big, with free POS software and hardware, as well as minimal (with the Free POS program) to no (with the Free Processing program) credit card processing fees.

Get started today with eHopper software and merchant service programs to cut costs and grow your revenue.